Legacy models in banking generally refers to older or pre-existing models that were originally built for credit risk management, regulatory capital (Basel II/III), or internal risk purposes, and which were later adapted for Expected Credit Loss (ECL) estimation under IFRS9.

In the banking world of financial risk management, regulatory frameworks like IFRS9 (International Financial Reporting Standard 9) have reshaped the way banks and financial institutions measure and recognize credit risk. Introduced in 2018, IFRS 9 replaced the incurred loss model under IAS 39 with a forward-looking expected credit loss (ECL) approach. While IFRS9 is built to be more responsive and realistic, many institutions continue to operate with legacy models – older models or methodologies that were built before IFRS9 but are still in use in some capacity.

What Are Legacy Models in Banking?

Legacy models in banking industry refer to pre-existing statistical, rule-based, or judgment-driven credit risk models that were primarily designed for frameworks like IAS 39 or internal portfolio management. These could include:

- Vintage analysis models: Tracking loan performance by origination cohort.

- Roll rate models: Estimating probabilities of migration between delinquency buckets.

- Static loss rate approaches: Using historical averages to predict future losses.

- Simplified provisioning models: Based on regulatory provisioning norms rather than expected credit loss.

Such models were retrospective and often relied on incurred losses—losses recognized only when default indicators became evident.

Why Legacy Models Still Exist in the IFRS9 World

Despite inclination of IFRS9 models toward forward-looking ECL, legacy models persist for several reasons:

- Data Limitations: Many banks, especially in emerging markets, lack sufficient long-term or granular datasets to fully support complex IFRS9-compliant models. Legacy models, which rely more on historical averages, remain practical in such cases.

- Regulatory Guidance: Regulators in certain jurisdictions allow transitional arrangements, permitting the use of adapted legacy models while banks gradually build IFRS9-ready frameworks.

- Cost and Resource Constraints: Building advanced probability of default (PD), loss given default (LGD), and exposure at default (EAD) models requires significant investment in data infrastructure, model development, validation, and governance. Smaller banks often rely on modified legacy models due to cost pressures.

- Comparability and Continuity: Legacy models in banking provide a continuity bridge. Institutions often benchmark their IFRS9 models against legacy models to assess stability, explain model shifts, and ensure stakeholders understand the transition.

Legacy Models vs. IFRS9-Compliant Models

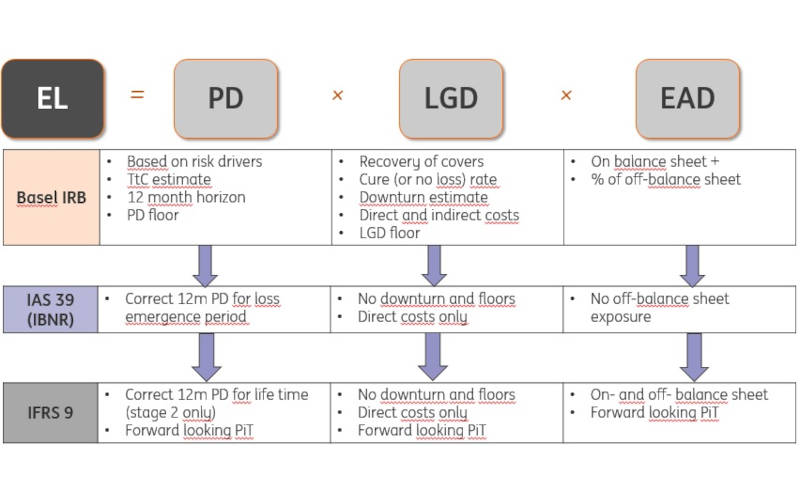

| Aspect | Legacy Models (IAS 39 style) | IFRS 9 Models |

| Loss Recognition | Incurred loss (reactive) | Expected loss (forward-looking) |

| Inputs | Historical delinquency & averages | Probability-weighted scenarios, macroeconomic overlays |

| Complexity | Simple / rule-based | Advanced statistical, often hybrid with expert judgment |

| Use of Macroeconomics | Minimal | Mandatory forward-looking macroeconomic scenarios |

| Provisions Impact | Lower, smoother provisions | Higher volatility due to scenario-based ECL |

| Regulatory Acceptance | Widely accepted pre-2018 | Mandatory under IFRS9 |

Role of Legacy Models Under IFRS 9

While the IFRS9 framework looks into forward-looking models, legacy models in banking still play supporting and transitional roles:

- Benchmarking and Backtesting: Banks often compare IFRS 9 results against legacy models to check reasonableness, highlight outliers, and ensure provisions are not overly conservative or aggressive.

- Scenario Stress Testing: Legacy roll-rate or static loss models are still used in stress testing to provide alternative perspectives and sanity checks.

- Data Gap Management: Where forward-looking data is unavailable, legacy models help plug gaps, especially for smaller portfolios or low-default portfolios.

- Internal Management Reporting: Senior management often prefers legacy model outputs for consistency with historical reporting, even if IFRS9 outputs are used for regulatory disclosures.

Challenges of Using Legacy Models in IFRS9

Despite the relevant benefits that legacy models in banking have to offer in today’s model landscape, there persists some challenges.

- Regulatory Compliance Risk: Over-reliance on legacy models risks non-compliance, as IFRS9 explicitly requires forward-looking expected loss measurement.

- Model Risk and Governance: Legacy models may not be subject to the same rigorous governance, validation, and documentation requirements as IFRS 9 models, creating operational risk.

- Stakeholder Misalignment: Different results from legacy and IFRS 9 models can cause confusion among auditors, regulators, and management.

- Reduced Relevance: Legacy models often fail to capture the effects of economic cycles and shocks—making them less predictive in volatile environments like COVID-19.

- Staging: Legacy models may not capture significant increases in credit risk (SICR) effectively.

The Way Forward: Integrating Legacy Models with IFRS9

Legacy models in banking are unlikely to disappear completely in the short term. Instead, banks are adopting a hybrid approach:

- Overlay Use: Using legacy roll-rate models as overlays or challengers to IFRS9 ECL outputs.

- Model Benchmarking: Maintaining legacy models as a parallel system to ensure reasonableness of IFRS9 provisions.

- Gradual Migration: Enhancing legacy models incrementally with forward-looking adjustments, until they evolve into full IFRS9 models.

- Data Infrastructure Investments: Building richer datasets to reduce reliance on legacy methodologies over time.

Conclusion:

Standing today, legacy models in banking continue to have a complementary role in the IFRS9 framework. While they are no longer sufficient as standalone tools for regulatory compliance, they still provide valuable contributions for benchmarking, back-testing, and even in transitional support. The ultimate goal for financial institutions should be a gradual but steady move toward robust, forward-looking, data-driven IFRS9 models—while leveraging legacy models as a safety net for reasonableness and transparency. Thus, in a rapidly evolving risk management landscape, legacy models in banking not only represent the past but also serve as a foundation on which the future of regulatory modeling is being built.